Author: John Mattiacci | Owner Mattiacci Law

Published April 17, 2026

TL;DR: Yes, you can file a personal injury claim without a police report in Philadelphia, but the missing report makes the case harder and requires immediate action. In Pennsylvania, a police report is not required to start a claim or lawsuit, yet claims without one often take 20 to 30% longer to process, and insurers look for reasons to challenge fault and damages.

You got home after the crash, adrenaline wore off, and now the questions are hitting all at once. No officer came. No report was made. The other driver seemed cooperative at the scene, but now they’re not answering. Or worse, the insurance company already sounds skeptical.

That situation is common, and it’s fixable. But you have to treat the lack of a police report as a problem you solve with evidence, not hope.

Insurers use a missing report as an advantage. They argue the crash may not have happened the way you say. They question whether your injuries came from this incident. They try to turn a straightforward claim into a credibility fight. If you want to know “Can I File Claim Without Police Report in Philly,” the answer is yes, but only if you build the file the police report would have helped create.

The Answer is Yes But You Must Act Fast

You get home from a crash in Philly, check your phone, and realize no officer ever came. By the time the soreness sets in, the other driver has gone quiet and the insurer is already asking careful questions. That is the moment a lot of valid claims start to weaken.

Yes, you can still file an insurance claim or a lawsuit without a police report in Pennsylvania. The problem is not whether you are allowed to file. The problem is what the insurance company does with that missing report. Adjusters use the gap to argue there is no neutral record of the scene, no early confirmation of fault, and no clean timeline tying your injuries to the crash.

That is why speed matters. In a no-report case, the first version of events that gets documented often shapes the whole claim.

What needs to happen right away

Start building the file the police did not create. Focus on proof that answers the three questions insurers usually attack first: how the crash happened, whether you were hurt, and whether the damage matches the impact.

Preserve every piece of physical and digital evidence

- Save photos, videos, dashcam footage, text messages, call logs, repair estimates, rideshare trip data, and witness names.

- Keep damaged property. A cracked helmet, torn jacket, child car seat, or broken phone can help show force and point of impact.

- Back everything up in one place so nothing gets lost or overwritten.

Get medical care and describe the cause clearly

- Prompt treatment creates a record close in time to the crash.

- Tell the provider where you hurt, when the symptoms started, and that the injuries followed the accident.

- If you wait too long, the adjuster will argue the condition came from work, a prior injury, or daily life.

Notify insurance without giving them extra ammunition

- Report the crash promptly.

- Stick to facts you know. Time, location, vehicles involved, and visible injuries.

- Do not guess about speed, apologize, or give a recorded statement that goes beyond the basics before you understand your injuries.

Here is the practical trade-off. Filing fast helps protect the claim, but talking too freely can damage it. The right approach is fast notice, careful wording, and strong documentation.

I tell clients this all the time: without a police report, credibility is not assumed. It has to be built. If you need the larger process, this guide on how to file a personal injury claim explains the steps. In a Philly no-report case, those steps matter more because you are creating the record yourself.

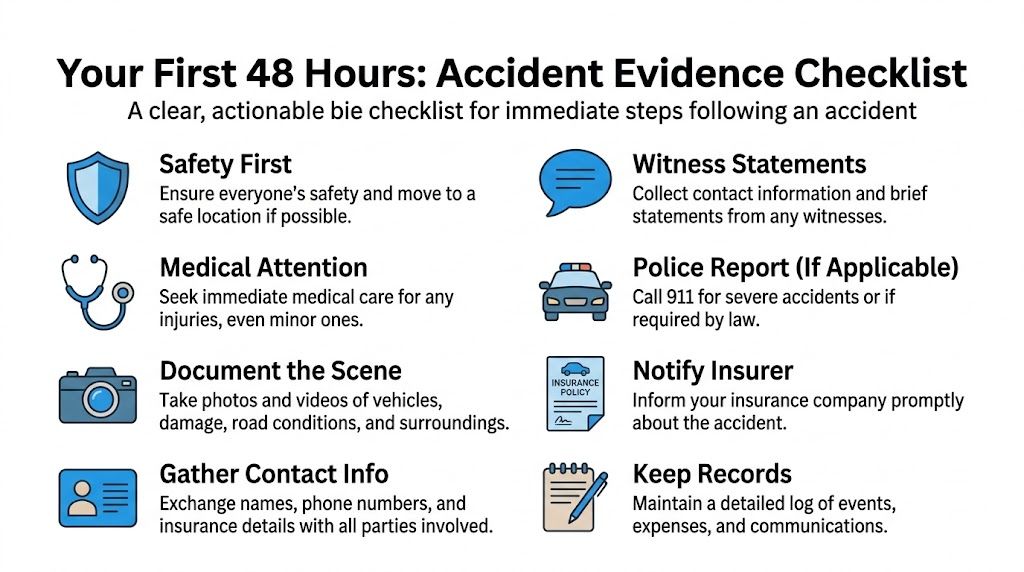

Your First 48 Hours Evidence Checklist

The strongest no-report claims are built fast. Not fancy. Fast.

A claimant-provided evidence package with photos, witness information, and medical records can still produce an 85% settlement rate in Pennsylvania, but delayed reporting can cause up to 40% of these claims to be rejected, according to Progressive’s explanation of filing without a police report.

That tells you exactly what the first two days are about. You are creating the record yourself.

What to collect at the scene or as soon as you safely can

Photos from every angle

- Get close shots and wide shots.

- Include vehicle damage, debris, skid marks, lane markings, intersections, traffic lights, weather conditions, and anything obstructing visibility.

People information

- Get the other driver’s name, phone number, insurance carrier, policy information, license plate, and driver’s license details if possible.

- If there are passengers, get their names too.

Witness contact details

- Ask for phone numbers and email addresses.

- A witness who says “call me if you need me” but doesn’t give full contact information often disappears.

Your own memory

- Write down what happened before details blur.

- Note direction of travel, traffic flow, signals, road position, speed estimates if known, and anything said by the other driver.

What to preserve after you leave

Some of the best evidence in these cases isn’t dramatic. It’s ordinary and consistent.

Save every receipt, every urgent care discharge paper, every towing invoice, every pharmacy printout, and every email with the insurer.

That paper trail helps prove both causation and damages.

A short checklist helps:

| Item | Why it matters |

|---|---|

| Medical records | Connects injury to the incident |

| Repair estimates | Shows force and property damage |

| Prescription records | Supports treatment timeline |

| Work absence records | Helps prove lost income |

| Ride-share or towing receipts | Shows disruption immediately after the event |

What people often get wrong

A lot of clients think the photos of the bumper are enough. They aren’t. The adjuster will want the whole context.

Another mistake is waiting to “see if it gets better” before going to a doctor. That gap becomes part of the defense story. They’ll say if you were really hurt, you would have sought care sooner.

For a more detailed breakdown of what to gather, this page on how to document evidence after a car accident is useful. In no-report claims, that documentation isn’t extra. It’s the backbone of the case.

Filing a Report After the Accident

A lot of people assume they can just call the police station later, explain what happened, and get a report started. In Philadelphia, it doesn’t work that way.

For injury incidents, you must go to a police district in person. You can’t file the report online or by phone, and processing delays can take 1 to 2 weeks, according to Rosen Justice on reporting an accident in Philadelphia.

What a late report can and cannot do

A late report can help create an official record that you complained of the crash and took steps afterward. That has value.

But it won’t do what an on-scene report sometimes does. The officer usually won’t have the vehicles in place, the witnesses standing there, or the same ability to observe damage and road conditions in real time. That means the report may document your account, but it may not resolve the dispute the way people hope.

Why insurers still attack late reports

Adjusters often treat late reports as weaker because the officer didn’t witness the aftermath close in time to the event. That gives them room to argue:

Memory problems

- They may say your recollection changed after talking to others.

Injury inflation

- They may claim you reported pain only after speaking with a lawyer or doctor.

Fault uncertainty

- They may argue there was no independent basis to assign blame.

A late police report can help. It just can't replace scene evidence, witness preservation, and prompt medical documentation.

If you’re physically unable to get to the district right away, don’t let that stop the rest of the claim work. Build the file with medical records, photos, witness statements, and property damage evidence while that report is pending.

Dealing With Insurers When You Have No Police Report

Many valid claims lose value. Not because the injured person is wrong, but because the insurer spots an opening and presses it.

Without a police report, insurers deny or undervalue claims up to 40% more often, and the average car accident claim value can drop from $25,000 to $18,000, according to Blackwell Attorneys on claims without police reports.

The three tactics adjusters use most

They turn it into a credibility fight

If there’s no officer narrative, the adjuster may frame the case as nothing more than your word against the other driver’s. That’s the classic “he said, she said” setup.

Your response is evidence that doesn’t depend on your memory alone. Time-stamped photos, treatment records, witness statements, surveillance requests, and repair documentation all help shift the discussion from opinions to proof.

They ask for too much talking and not enough documents

Recorded statements are a favorite tool in no-report cases. The adjuster sounds polite, but the goal is often to lock you into phrasing they can use later.

Keep communications tight. Basic facts are enough early on.

Give dates and locations

- Be accurate and brief.

Don’t speculate

- If you don’t know speed, distance, or timing, say you don’t know.

Don’t minimize injuries

- Saying “I’m fine” on day one can come back to haunt you if symptoms worsen.

They make a quick offer before the file is complete

A weak early offer often signals that the insurer thinks your proof is thin. In no-report claims, they may assume pressure will make you settle before the evidence develops.

If you need a practical primer on response strategy, this article on how to negotiate with insurance adjusters is helpful for understanding the back-and-forth. The same principle applies here. Organization and restraint beat emotion.

What works better than arguing

A clean claim package does more than angry phone calls ever will.

| Insurer tactic | Better response |

|---|---|

| “We can’t verify fault” | Send photos, witness contacts, scene notes, and repair proof |

| “Your injuries may be unrelated” | Provide prompt medical records and treatment timeline |

| “We need your recorded statement now” | Respond in writing and keep facts limited |

| “This is our best offer” | Evaluate the file first, then answer with documented support |

If the adjuster keeps circling back to the missing report, that’s usually a sign they don’t like the rest of your evidence. Keep building that evidence.

Pennsylvania Deadlines and Your Right to Sue

A common mistake in no-report cases is assuming the insurance claim keeps the legal clock paused. It does not.

You can keep negotiating with the carrier for months, send records, answer questions, and still lose your right to file suit if the deadline expires. In Pennsylvania, personal injury claims are generally governed by a two-year filing deadline under 42 Pa.C.S. § 5524. If you want a plain-English breakdown of how that deadline works, read this guide to the Pennsylvania car accident statute of limitations.

That deadline matters even more when there is no police report.

Here is why. The missing report gives the insurer room to stall. Adjusters ask for one more statement, one more medical update, one more round of review. Meanwhile, the defense is not trying to help you build the case. It is testing whether time will solve the problem for them.

I see this often. A person thinks the claim is active, so everything is fine. Then the carrier denies fault at month twenty-three, or makes a low offer knowing there is very little time left to file.

The practical split is simple:

Insurance claim

- A request for benefits or payment from the carrier

- Handled outside court

- Can stay open while the statute keeps running

Lawsuit

- A formal court filing

- Preserves your right to pursue damages if settlement fails

- Must be filed on time, even if talks with the insurer are still going

Without a police report, filing deadlines become part of claim strategy, not just calendar management. If the insurer knows you are close to the deadline and unprepared to sue, your bargaining power diminishes quickly. If your case is documented, investigated, and ready to file before the clock runs out, the conversation changes.

Why No-Report Claims Need an Investigator and Trial Lawyer

A no-report claim can look manageable at first. Then the insurer starts pressing on the gaps.

No officer narrative means no neutral summary of fault, no diagram, and usually no ready-made witness list. The carrier uses that absence in predictable ways. It argues the crash is unclear. It questions whether the injuries came from this accident. It treats every missing detail as a reason to pay less or deny the claim outright.

That is why these cases need more than paperwork. They need proof gathered fast and put in a form that can survive a lawsuit.

What lawyers do in these cases

The work starts with building the record the police report would have helped create, and then going further.

A serious no-report case may require:

Scene reconstruction

- Using vehicle damage, final positions, measurements, photos, and roadway design to show how the crash happened.

Witness development

- Finding witnesses early, getting signed statements, and preserving testimony before memory slips or people stop responding.

Video preservation

- Sending preservation requests to stores, homes, parking lots, SEPTA-adjacent properties, or nearby buildings before footage is deleted.

Medical causation framing

- Organizing treatment records, prior history, and timeline evidence so the insurer has less room to argue that something else caused the injury.

That work changes the case. It also exposes weak spots early. If liability is thin, a good trial lawyer will say so. If the proof is there, the file gets built for court, not just for an adjuster.

Why trial preparation changes negotiations

Insurers know the difference between a claim that is being discussed and a claim that is being prepared for trial.

When the file shows preserved video requests, identified witnesses, complete medical records, and a liability theory that can be defended under oath, the defense has to take the case more seriously. If the file is thin, delays and low offers usually follow.

Mattiacci Law handles serious injury litigation in Pennsylvania and New Jersey and works with medical and accident reconstruction experts when a case needs independent proof of fault and damages.

The missing police report does not end the case. It means the case has to be proved from the ground up.

If fault is disputed, the injuries are significant, or the insurer is already pushing back, handling a no-report claim alone can get expensive fast.