Author: John Mattiacci | Owner Mattiacci Law

Published May 5, 2026

You’re probably reading this after the adrenaline wore off.

The crash happened fast. One second you were trying to get through Philly traffic. The next, you were dealing with police, a tow truck, a wrecked car, and a phone full of missed calls. Now the headache starts. Your neck hurts. Your car is in a lot somewhere. An insurance adjuster wants to “just get your side.” You’re wondering whether you’re supposed to call your own insurer first, what Pennsylvania no-fault means, and whether saying the wrong thing is about to cost you money.

That anxiety is justified. Handling insurance after a car accident in Philadelphia isn't simple because Pennsylvania doesn't use a clean, easy system. It uses a choice no-fault setup, and that creates traps. Your own policy matters. Your tort election matters. The other driver's coverage matters. What you say in the first call matters. In Philly, adjusters know many drivers are overwhelmed and they use that.

If you want the blunt version of How to Handle Insurance After a Car Accident Philly, here it is: get medical care, lock down evidence, report the claim carefully, and stop talking before an adjuster turns your uncertainty into their defense.

The Shock Has Worn Off Now What

The first night after a crash is usually worse than the scene itself.

At the scene, you’re moving on instinct. You answer questions. You call family. You stare at the damage and barely process it. Later, when the apartment is quiet or you’re sitting in your kitchen with discharge papers and a tow receipt, everything hits at once. Your body stiffens up. You start replaying the crash. You wonder whether you should’ve said less, taken more photos, or gone straight to the ER.

That’s a normal reaction. What isn’t normal is how much pressure insurers put on people in that window. They know you’re tired, rattled, and trying to be cooperative. They also know most Philly drivers don’t have a clear grasp of what their own policy says.

Philly crashes create legal problems fast

In Pennsylvania, your own auto policy usually has to start paying first for medical treatment through Personal Injury Protection, often called PIP or first-party benefits. Pennsylvania requires at least $5,000 in PIP and uses a choice no-fault system, which means your own coverage pays initial medical bills regardless of fault, while your tort election affects whether you can pursue pain and suffering claims later, as explained in this breakdown of Pennsylvania car insurance rules and tort choices.

That sounds simple until real life gets involved.

A lot of people don’t know whether they picked Full Tort or Limited Tort. They don’t know their liability limits. They don’t know whether they bought UM/UIM coverage for uninsured or underinsured drivers. They definitely don’t know how an adjuster will use a casual statement like “I’m probably okay” once their symptoms get worse.

Practical rule: The insurance process starts building against you before you understand your injuries.

Don’t treat this like paperwork

This isn’t just a property damage issue unless all you lost was a bumper and a few hours of your day. If you’re sore, dizzy, missing work, or getting calls from insurers, you’re already in claim territory where mistakes matter.

Here’s the mindset I recommend:

- Think medically first: Your body matters more than your car.

- Think strategically second: Every document, photo, and statement can help or hurt your claim.

- Think skeptically about insurers: Friendly doesn’t mean neutral.

- Think locally: Philly claims are shaped by Pennsylvania rules, not by what your cousin in another state told you.

If you’re stressed, good. Not because stress is helpful, but because it means you understand this matters. The fix is structure. You need to know what to do in the first day, what to say to insurance, and when to stop handling it yourself.

Your First 24 Hours Critical Actions and Evidence

The first day is where people either protect their claim or compromise it.

You don’t need to be perfect. You do need to be disciplined. Under Pennsylvania law, drivers must report accidents promptly to their insurer, and evidence like photos, witness information, and police reporting matters because insurers try to shift blame under modified comparative negligence, where recovery is allowed only if you’re 50% or less at fault, as outlined in this guide on reporting an insurance claim after a Philadelphia car accident.

At the scene do less talking and more documenting

Drivers often talk too much after a crash. They apologize. They guess. They try to smooth things over. That’s a mistake.

Do this instead:

- Get medical help if there’s any chance you’re hurt. If someone is injured, if there’s a death, or if a vehicle needs towing, police reporting is mandatory. Call 911.

- Photograph the whole scene. Not just the dent. Get lane positions, intersections, traffic signs, debris, skid marks, weather, and every side of the vehicles.

- Get witness names and contact details. Witnesses disappear fast.

- Exchange only necessary information. Name, insurance, registration, license, and vehicle details.

- Say nothing about fault. Not “I’m sorry.” Not “I didn’t see you.” Not “maybe I was going too fast.”

If the other driver wants to “handle it off the books,” assume that offer disappears the moment bills show up.

In the hours after the crash build your file

Once you leave the scene, start acting like you may need to prove every part of your claim later.

Create one folder on your phone and one folder in your email. Put everything there. Photos, tow paperwork, discharge papers, prescriptions, rental receipts, and the names of every doctor or urgent care provider you saw.

A few practical moves matter a lot:

- Get checked out promptly: Delayed treatment gives insurers room to argue your injuries came from something else.

- Write down symptoms the same day: Neck pain, headache, numbness, back stiffness, dizziness, trouble sleeping.

- Keep damaged items: Child seats, broken glasses, bloodied clothing, damaged electronics.

- Tell your employer if you miss time: Save emails, texts, and payroll records.

If the crash involved a commercial vehicle, the response gets more technical fast. This practical guide to commercial truck accident response is useful because truck cases often involve extra records, company reporting, and preservation issues beyond a standard two-car wreck.

Use a simple checklist, not memory

You’re not going to remember everything clearly the next day. Use a checklist and fill it out while it’s fresh.

- Scene proof: Photos, video, location, weather, vehicle damage

- People involved: Drivers, passengers, witnesses, responding officers

- Medical trail: ER, urgent care, prescriptions, symptoms

- Paper trail: Tow, storage, repair estimate, claim number

- Next-step guide: Review this Philly-specific checklist on what to do immediately after an accident in Philly

The point of all this isn’t overkill. It’s your advantage. If an adjuster later claims you caused the crash or weren’t really hurt, your evidence is what pushes back.

Understanding PAs Unique Insurance Rules

Pennsylvania confuses drivers because it mixes no-fault features with fault-based claims. People hear “no-fault” and assume that means they can’t recover from the driver who caused the crash. That’s wrong. They also assume all policies work the same. Also wrong.

The three pieces that matter most are PIP, Full Tort, and Limited Tort.

PIP pays first whether you caused the crash or not

Pennsylvania requires a minimum of $5,000 in PIP for immediate medical costs, which means your own policy usually covers initial treatment regardless of fault, as described in this explanation of Pennsylvania PIP and tort election rules.

That’s the practical meaning of no-fault here. You don’t wait for the other carrier to accept blame before getting some medical bills paid. You open a first-party claim with your own insurer.

That doesn’t mean PIP is enough. It often isn’t.

Moderate to serious injuries can burn through $5,000 fast. Once those benefits are exhausted, the rest of the claim shifts into other coverage questions, including the at-fault driver’s liability insurance and, in some cases, your own uninsured or underinsured motorist coverage.

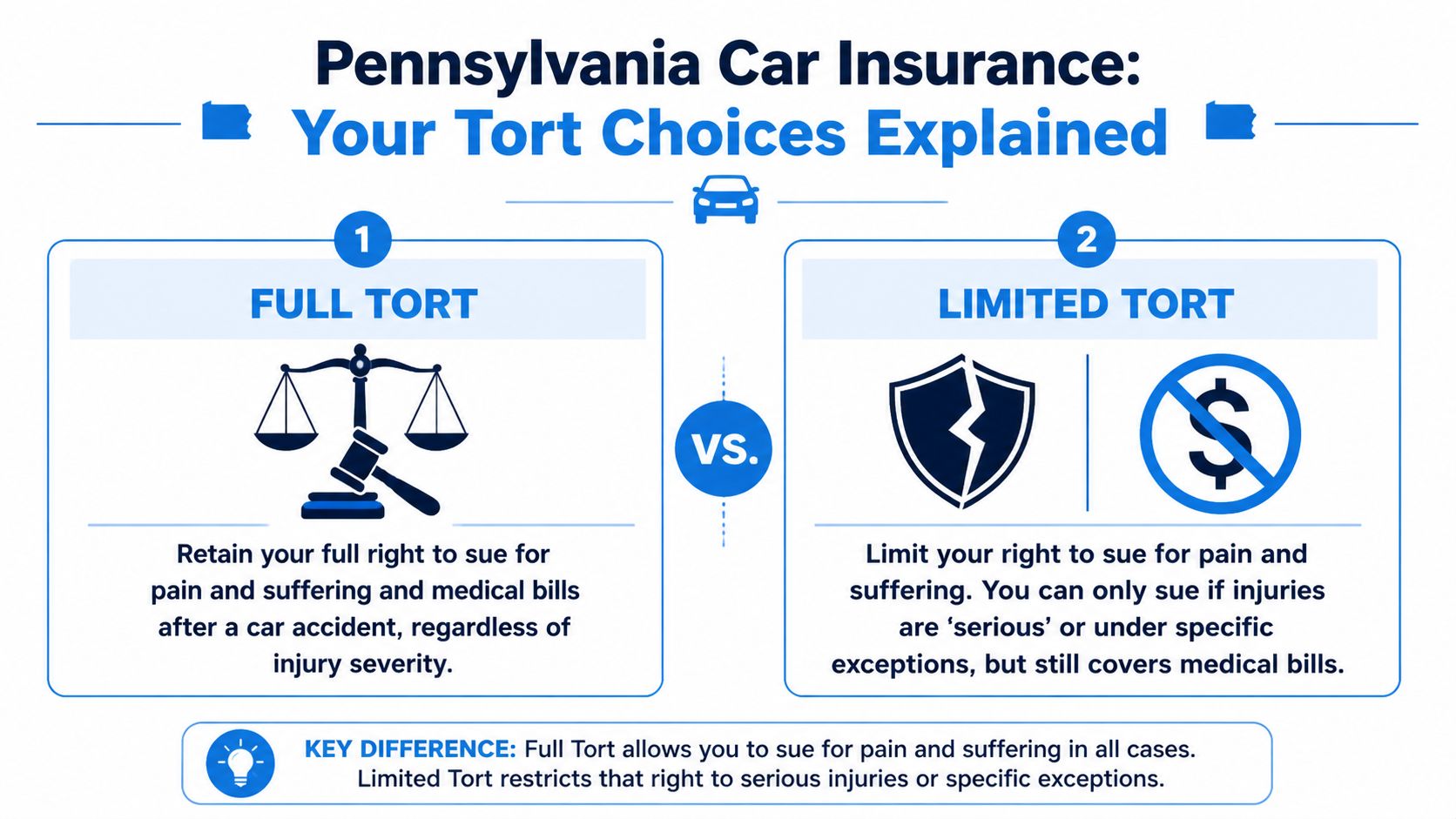

Full Tort and Limited Tort are not a minor detail

Pennsylvania drivers frequently get blindsided.

Full Tort preserves your right to pursue pain and suffering damages without that extra threshold fight. Limited Tort restricts that part of the claim unless the injury qualifies as serious under the law. That sounds technical, but its practical effect is simple. A choice you made years ago to lower premiums may now be limiting what you can recover.

Here’s the clean comparison:

| Option | What it means after a crash |

|---|---|

| Full Tort | You keep your full right to seek pain and suffering damages. |

| Limited Tort | You may still recover medical-related losses, but pain and suffering claims are restricted unless the injury meets the serious threshold. |

Limited Tort is where insurance companies get aggressive. They don’t just challenge fault. They challenge whether your injury counts enough.

Liability limits and UM UIM matter in Philly

Pennsylvania’s minimum liability coverage is 15/30/5, meaning $15,000 per person, $30,000 per accident, and $5,000 for property damage, according to the same Pennsylvania insurance framework discussed earlier in the article. That may satisfy the law, but it doesn’t go far in a meaningful injury case.

This is why UM/UIM coverage matters. If the driver who hit you has too little insurance or none at all, your own policy may be the only real backstop. In the verified example, if your medical bills reach $30,000 and the at-fault driver only has $15,000 in bodily injury coverage, underinsured motorist coverage can step in up to your policy limits.

One document answers half your questions

Pull your declarations page. Today.

That page tells you what you bought. It will show your tort election, your PIP amount, and whether you carry UM/UIM. If you don’t know those answers before speaking with adjusters, you’re negotiating in the dark.

Reporting the Accident and Filing Your Claim

At this point, people either stay in control or hand control to the insurance company.

You have two separate insurance conversations after a Philly crash. One is with your own insurer to get the claim opened and start first-party benefits. The other is with the other driver’s insurer, which is the conversation most likely to hurt you if you handle it casually.

Report your own claim quickly and keep it basic

To start your claim, file for PIP with your own insurer right away. When giving your Notice of Loss, stick to basic facts like the date, location, and vehicles involved, and avoid speculation. Insurers use recorded statements to reduce payouts, especially when they come from the other driver’s carrier, as explained in this guide on the steps to take after a car accident that wasn’t your fault.

Your own carrier needs enough information to open the file. They do not need your theories.

Use something like this:

“There was a collision on [date] at [location]. The vehicles involved were [basic vehicle information]. Police responded. I’m seeking medical evaluation and I need to open my first-party benefits claim.”

That does the job. It opens the file without giving them extra material to pick apart.

What to say and what not to say

Here’s the rule. Facts, not guesses.

Say:

- Date and place: When and where it happened

- Vehicles involved: Make, model, and who was driving

- Police response: Whether officers came to the scene

- Medical status: That you’re being evaluated or treated

Do not say:

- Fault opinions: “I think I may have caused it”

- Speed estimates: Unless you know them with certainty and have a reason to state them

- Injury minimizers: “I’m fine” or “just sore”

- Speculation: “Maybe the light had just changed”

The other driver’s adjuster is not your helper

When the other carrier calls, slow everything down.

You are not required to help them build their defense. You are not required to give a recorded statement to the other driver’s insurance company just because they ask. In fact, I recommend you decline.

Use a short script:

- Basic response: “I’m not prepared to discuss details of the crash.”

- Recorded statement response: “I’m not giving a recorded statement.”

- Medical response: “I’m still being evaluated.”

- Paperwork response: “Send any requests in writing.”

That’s enough. You don’t win these calls by sounding nice. You win by giving them nothing they can twist.

Keep the claim organized like a case file

Treat this like a running file from day one. If you don’t, details get lost and insurers benefit.

Use a simple structure:

| Item | What to save |

|---|---|

| Claim info | Claim number, adjuster name, phone, email |

| Medical records | Visit summaries, prescriptions, referrals, bills |

| Vehicle records | Tow slips, repair estimates, total loss paperwork |

| Work loss proof | Employer notes, missed shifts, pay records |

| Communication log | Date, time, and summary of every insurance call |

One practical point matters more than people think. Don’t sign broad releases just to “move things along.” Insurers love broad authorizations because they give the company more paper than it needs and more opportunities to attack your claim.

Navigating Lowball Offers and Adjuster Tactics

The first settlement offer is often designed to end the claim cheaply, not fairly.

That’s not me being cynical. That’s how the system works. Adjusters are trying to close files before the full medical picture develops, before your wage loss is clear, and before you understand what your case may involve under Pennsylvania law.

Philadelphia claims are especially prone to this because insurers move fast and count on volume. They know a lot of injured drivers just want the calls to stop.

What adjusters are really doing

When an adjuster offers money early, they’re usually buying certainty from you while you’re still living with uncertainty.

You may not know yet whether your pain will resolve, whether you’ll need specialists, whether your car will be totaled, or whether your missed work will continue. The adjuster knows that. That’s exactly why early offers happen.

A quick check feels like relief. It can also be the cheapest exit the insurer will ever get.

Common Insurance Adjuster Tactics and How to Respond

| Adjuster Tactic | What It Means | Your Best Response |

|---|---|---|

| Recorded statement request | They want to lock you into wording before facts and treatment are clear. | Decline and ask for requests in writing. |

| Fast settlement offer | They want closure before you know the true value of the claim. | Don’t discuss settlement until treatment and damages are clearer. |

| Blaming you for the crash | They’re trying to reduce or defeat recovery through comparative fault arguments. | Stick to evidence, not memory-based guesses. |

| Downplaying your injury | They’re testing whether you’ll back off because damage “doesn’t look serious.” | Let records, doctors, and treatment speak for the injury. |

| Pressure deadlines | They want urgency on their timeline, not yours. | Slow it down and request everything in writing. |

| Broad medical authorizations | They want access to more history than they need. | Don’t sign broad releases without legal review. |

Don’t negotiate from pain and panic

A lot of people accept bad offers because they’re tired. That’s understandable. It’s also expensive.

Minor injuries may resolve with limited treatment, while serious injuries can involve much larger claims. The verified data shows minor soft-tissue injuries might settle for $5,000 to $25,000, while cases requiring surgery or causing permanent limitations often exceed $100,000, as noted in this Philadelphia-focused overview of insurance handling after a car accident.

That range is exactly why rushing is dangerous. If you settle before you know where your injury falls, you’re guessing with your own money.

Build pressure with proof not outrage

You don’t beat an insurer by telling them they’re unfair. You beat them with documentation.

Use:

- Medical records: Consistent treatment and diagnosis

- Bills and receipts: Every out-of-pocket cost

- Wage loss proof: Missed work and reduced earning

- Photos and scene evidence: Damage, injuries, and context

- Symptom journal: A plain, dated account of what the injury is doing to your life

If an adjuster acts offended because you won’t jump at the first number, ignore the performance. Their job is to save the company money. Your job is to avoid making their job easy.

When You Absolutely Need a Philly Car Accident Lawyer

A Philadelphia adjuster sounds friendly right up until your claim gets expensive. Then the tone changes. They start blaming a prior injury, arguing you were partly at fault, or acting like your Limited Tort election blocks recovery when it may not.

That is the point to stop treating this like paperwork.

Some claims stay small and straightforward. The serious ones do not. If you have real injuries, a fault dispute, or a coverage problem under Pennsylvania’s insurance rules, handling the claim yourself can cost you far more than a lawyer ever will.

Get legal help if any of these are happening:

- You suffered a serious injury: ER care, hospitalization, surgery, broken bones, a concussion, herniated discs, or lasting physical limits

- The insurer disputes fault: They say you caused the crash, share blame, or question the police report

- Your Limited Tort status matters: Pennsylvania’s choice no-fault system can limit pain and suffering claims, but there are exceptions, and insurers count on people not knowing them

- There is an uninsured or underinsured driver: UM and UIM claims turn into policy language fights fast

- Your symptoms showed up later: Neck, back, and head injuries often get worse after the adrenaline wears off

- The carrier is delaying, denying, or pressuring you: Repeated document requests, broad medical releases, sudden silence, or a rushed settlement offer are all warning signs

These cases go bad for predictable reasons. Causation gets challenged. Coverage gets read as narrowly as possible. Philadelphia insurers also use comparative negligence arguments to shave down payouts, even in crashes that look obvious at first.

The release is another trap.

Once you sign it, your claim is usually over. If an MRI later shows more damage, if you end up needing injections or surgery, or if your missed time from work grows, the insurance company will still say the case is closed. They got certainty cheap. You took the risk.

Mattiacci Law is a Philadelphia personal injury firm that handles insurer communication, investigates serious crash claims, and files suit when a carrier refuses to pay fairly.

If the insurer is fighting over fault, injury severity, delayed symptoms, Limited Tort, or available coverage, you are in a legal dispute. Treat it that way.