Author: John Mattiacci | Owner Mattiacci Law

Published March 16, 2026

When someone hits your car and you're left with injuries and medical bills, the first few minutes at the scene are everything. What you do—and what you don't do—can make or break your ability to get fairly compensated later. These initial steps are the bedrock of your injury claim. They protect your health, your rights, and your financial recovery from the very beginning.

What To Do Right After The Crash

The moments after a car accident are a chaotic mix of adrenaline, confusion, and often, pain. It’s easy to feel completely overwhelmed, but the steps you take right here will have a huge impact on getting those medical bills paid down the road.

Your absolute first priority is safety. Check on yourself and your passengers. If you can, move your vehicle out of the flow of traffic to avoid a second collision.

And even if the crash seems minor, calling 911 is non-negotiable. A police officer showing up does two critical things for you. First, it gets medical help on the way for anyone who needs it. Second, it creates an official police report—an impartial document that becomes a cornerstone of your injury claim.

We've found that clients who take these first few steps seriously are in a much stronger position from day one. To make it easier, here is a quick-reference table of the most important actions to take.

Critical Post-Accident Action Plan

| Your Action | Why It's Essential for Your Case |

|---|---|

| Check for Injuries & Call 911 | Ensures immediate medical care and creates an official police report, which is key evidence. |

| Document the Scene Extensively | Photos/videos of damage, positions, and skid marks prevent the other driver from changing their story. |

| Exchange Information | Get the other driver's license, insurance, and contact details. This is necessary for filing a claim. |

| Get Witness Contact Info | A neutral third-party account can be incredibly valuable in proving who was at fault. |

| Watch What You Say | Avoid saying "I'm sorry" or "I'm okay." Adrenaline can mask injuries, and apologies can be used against you. |

| Seek Medical Attention | Go to the ER or an urgent care, even for "minor" pain. This creates a medical record linking your injuries to the crash. |

Taking these steps helps build a solid foundation for your case before evidence disappears or memories fade.

Document Everything at the Scene

Your smartphone is your single most powerful tool for collecting evidence. Don't just snap a few quick pictures of a dented bumper. You need to create a complete visual story of the entire scene before the cars are moved.

Think like an investigator and capture everything:

- Wide shots that show where all the vehicles ended up after the impact.

- Close-up photos of the damage to every car involved, taken from several different angles.

- Key details like skid marks on the pavement, broken glass or debris, and any nearby traffic signs or signals.

- The other driver's license plate, their driver's license, and their insurance card.

A quick video where you walk around the entire scene can also be incredibly powerful. It captures the full context in a way that static photos sometimes miss. This is the proof that helps establish who was at fault and shuts down any attempts by the other driver to change their story later.

Control the Conversation

When you talk to the other driver, your words matter—a lot. It’s a natural human instinct to be polite or even apologetic, but you have to resist the urge. Avoid saying things like "I'm sorry" or even "I'm okay." These statements can be twisted later to sound like you're admitting fault or claiming you weren't hurt. Right now, your adrenaline is probably masking the true extent of your pain.

Stick to the facts. Exchange your insurance and contact information calmly and politely. If the other driver gets angry or confrontational, just disengage and wait for the police. You are not required to debate how the accident happened with them.

Grabbing information from any witnesses is also a game-changer. A neutral, third-party story about what happened can be priceless. Make sure you get their name and phone number before they decide to leave.

For a more detailed checklist, see our guide on what to do immediately after a car accident in Pennsylvania. Once you've documented the scene and you're in a safe place, your next call should be to an experienced attorney who can start guiding you on how to handle your medical bills and protect your claim from the very start.

How to Handle Medical Care and Growing Bills

When you’ve been hit by another driver, your first thought is your health. But a close second is often the flood of medical bills that starts piling up. It’s a huge source of stress. The most important thing to remember is this: never put off seeing a doctor because you’re worried about who will pay.

The adrenaline from a crash is powerful. It can easily mask serious injuries like whiplash, concussions, or even internal damage. Getting checked out right away does two critical things: it gets you the care you need, and it creates a medical record that ties your injuries directly to the accident. That link is everything when it comes to getting your bills covered later on.

The Immediate Costs and Who Pays First

Right after a crash, the expenses can hit you fast. We’re not talking about bills that show up months later; these are immediate costs that can feel overwhelming from day one:

- Emergency room co-pays and facility fees

- X-rays, CT scans, or MRIs to diagnose your injuries

- Prescriptions for pain medication

- Follow-up visits with orthopedic doctors or neurologists

- The first few physical therapy or chiropractic sessions

So, who pays for all this? In a no-fault state like Pennsylvania, the answer might surprise you: your own auto insurance pays first. This is done through your Personal Injury Protection (PIP) coverage. It’s mandatory coverage for exactly this reason—to make sure your medical bills get paid right away, no matter who was at fault for the crash. You’ll need to open a PIP claim with your own insurance company to get the ball rolling.

Think of your PIP coverage as your first line of defense. It lets you get the treatment you need without having to wait weeks or months for the at-fault driver’s insurance company to finally admit their driver was responsible.

This is a crucial point. When you go to the ER or your doctor, you should give them your auto insurance information, not your health insurance card (at least not at first). To keep from getting hit with unexpected bills from your doctors, it’s also smart to understand concepts like balance billing.

What Happens When Your PIP Benefits Run Out

Here’s the problem: most drivers in Pennsylvania only carry the state minimum for PIP coverage, which is just $5,000. If you have any kind of significant injury, that money disappears fast. A single MRI and a few weeks of physical therapy can burn through that entire amount.

Once your PIP is gone, the responsibility for paying usually shifts to your private health insurance. But this is where things get messy. Your health plan likely has its own high deductibles and co-pays you'll have to cover. Even worse, they will almost certainly want to be paid back for everything they covered out of your final settlement. That process is called subrogation, and it can take a huge bite out of your compensation.

This is where having an experienced lawyer in your corner makes a real difference. We step in and negotiate with your medical providers to make sure your treatment continues, even after your PIP is maxed out. How? We get them to agree to a medical lien.

A lien is simply a formal agreement that lets you keep getting medical care now. In return, the provider agrees to wait for payment until your case is over, at which point they get paid directly from your settlement or jury award. It’s a powerful tool that keeps the billing headaches at bay so you can focus on getting better while we build your case. To dig deeper into this, you can learn more about how PIP affects your accident claim in Pennsylvania in our detailed guide.

Making Sense Of Your Insurance Coverage

After a crash, trying to figure out which insurance pays for what can feel like a total nightmare. You’ve got multiple policies in the mix, and each one has a specific job. Knowing the pecking order is the key to getting your medical bills paid without getting buried in debt.

Your first line of defense is always your own auto insurance policy—specifically, your Personal Injury Protection (PIP) if you're in Pennsylvania. This is your primary source for immediate medical bill payments, no matter who caused the crash. It’s designed to get you the treatment you need, right now.

What About the At-Fault Driver’s Insurance?

Once your own PIP benefits are maxed out, the attention turns to the driver who hit you. Their Bodily Injury (BI) liability insurance is on the hook for the rest of your damages. This isn’t just about covering your leftover medical bills; it also includes your lost wages and the real, human cost of your pain and suffering.

But don’t expect a check in the mail. The other driver’s insurance company isn’t your friend. You have to build a solid claim that proves their insured was at fault and clearly shows the full extent of your injuries and losses. It's an uphill battle. If you're trying to get a handle on the different policies at play, understanding your insurance options is a good place to start.

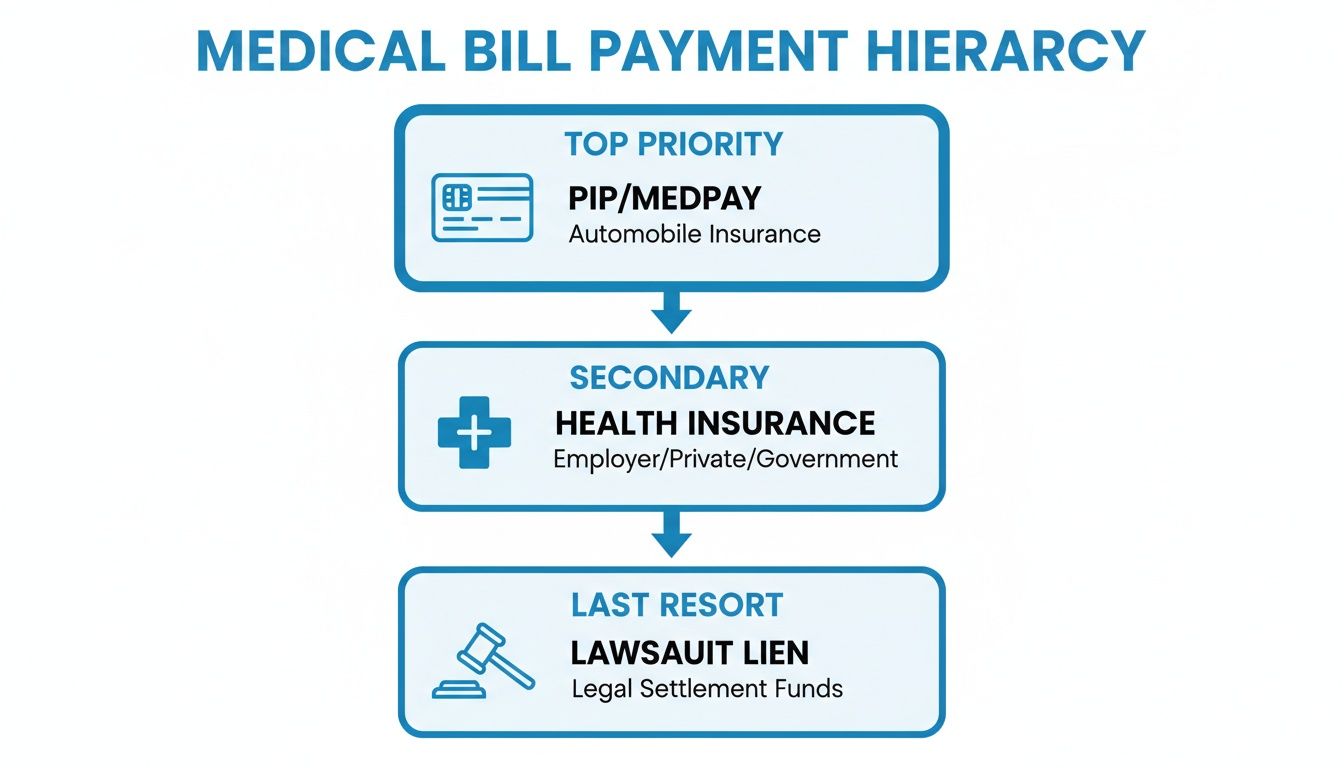

Here’s a look at the typical payment flow after a car accident.

As you can see, your own PIP benefits kick in first. After that, your health insurance might step in, with a lawsuit ultimately covering all remaining costs and liens from the final settlement.

The Critical Role of UM/UIM Coverage

What if the driver who hit you has no insurance? Or not enough to cover your mountain of medical bills? It’s a frighteningly common problem. In Pennsylvania alone, an estimated 6.5% of drivers are uninsured. This is where Uninsured/Underinsured Motorist (UM/UIM) coverage becomes an absolute lifesaver.

Let’s run through a real-world scenario we see all the time:

Imagine you get rear-ended and need back surgery. Your medical bills quickly shoot past $100,000. The at-fault driver only has the New Jersey minimum BI liability coverage of $25,000. Without UIM coverage on your own policy, you’d be stuck with $75,000 in unpaid bills—and get nothing for your lost income or pain and suffering.

Now, let's say you had the foresight to purchase $250,000 in UIM coverage. In that case, your own insurance company would step up and cover the $225,000 gap left by the other driver. That money would be available to pay your outstanding medical bills and compensate you for everything else you’ve lost.

This is why we drill it into every client: UM/UIM isn't some optional add-on. It's essential protection for you and your family. It guarantees there’s a path to financial recovery even if the person who hurt you was irresponsible. Making a UM/UIM claim can feel weird, almost like you’re suing yourself, but it's a benefit you paid for to protect yourself in exactly this type of disaster.

Determining The True Value Of Your Injury Claim

When someone hits your car and you're left with medical bills, it's easy to think your settlement is just about paying off that stack of papers. But that's a huge mistake.

The true value of your injury claim goes way beyond the bills you have today. To get what you actually deserve, you need to account for all the ways this accident has cost you—both financially and personally.

An experienced lawyer will break down your losses into two main buckets: economic and non-economic damages. Think of these as the tangible, receipt-based costs versus the very real, but intangible, human costs of the crash.

Calculating Your Economic Damages

Economic damages are all the losses that have a clear dollar amount tied to them. These are the financial hits you can prove with bills, pay stubs, and solid expert projections.

And it’s so much more than just the first ER bill. A full calculation of your economic damages includes:

- Past Medical Expenses: This covers every single bill you’ve racked up so far. We’re talking the ambulance ride, the hospital stay, co-pays for physical therapy, prescriptions—everything.

- Future Medical Needs: What if your doctor says you’ll need another surgery in two years? Or ongoing pain management for the rest of your life? A strong claim includes the projected cost of all future medical care, not just what you need right now.

- Lost Wages and Income: This is the money you lost from being out of work. It also covers any lost promotions, bonuses, or commissions you would have earned if you hadn't been injured.

- Loss of Future Earning Capacity: If your injuries mean you can’t go back to your old job or can't work at the same level, you are entitled to compensation for that diminished ability to earn a living over your lifetime.

The goal is to make you financially whole again, as if the accident never happened. This requires looking not just at what you’ve already lost, but what this injury will cost you for years to come.

The Value Of Your Pain And Suffering

Non-economic damages are just as real, but they don't come with a price tag. This is compensation for the human cost of the crash—the pain, the stress, and all the ways your life has been turned upside down.

This is where a skilled attorney builds a compelling story. We use your medical records, testimony from you and your family, and expert reports to show the insurance company the true impact.

It's about demonstrating the real-world consequences. Maybe you can't pick up your child anymore, had to give up a hobby you loved, or now deal with daily anxiety and trauma from the crash. These non-economic damages often represent a huge portion of a final settlement.

Understanding how lawyers build these arguments is key. You can learn more about how Philadelphia accident lawyers calculate car accident settlements in our detailed guide. It's not about a simple formula; it's about telling your unique story effectively to justify the compensation you need.

Why An Experienced Trial Lawyer Is Your Best Asset

When someone hits your car and you're suddenly buried in medical bills, it's easy to feel like you're on your own. You're not. But trying to take on an insurance company by yourself is an unfair fight from the start.

Their adjusters are professionals whose entire job is to protect their company’s profits. That means paying you as little as they can get away with. This is where bringing in an experienced personal injury lawyer completely changes the game.

Once we're on your side, the insurance company can no longer call you. All communication goes through us. This puts an immediate stop to their attempts to get a recorded statement or twist your words. It takes that weight off your shoulders so you can focus on one thing: getting better.

We Know the Insurance Company's Playbook

Insurance companies use a handful of tried-and-true tactics to minimize what they pay. A seasoned attorney has seen this playbook a thousand times and knows exactly how to shut it down.

Here are a few of the most common moves we see:

- The Quick, Lowball Offer: Days after the crash, an adjuster might call with a fast settlement offer. It’s tempting, but it’s a trap. This initial offer is always a fraction of what your claim is actually worth and rarely covers more than your first few bills. If you accept it, you give up your right to any future compensation, period.

- Delay, Delay, Delay: Adjusters are masters at dragging things out. They know that if they wait long enough, you might get frustrated, desperate, and accept a terrible offer just to be done with it.

- Twisting Your Words: Innocent comments like, “I think I’m okay,” or even a simple “I’m sorry,” can be used to argue you weren’t really hurt or that you admitted fault for the accident.

Our job is to act as your shield. We know their game because we play it every single day—only we play it for our clients.

The Power of Being Ready for Trial

Here's the honest truth: insurance companies write their biggest settlement checks when they know your lawyer is not afraid to take them to court. It’s a simple business calculation for them. The risk and expense of a jury trial are usually far greater than the cost of making a fair settlement offer.

A true trial lawyer doesn't just shuffle paperwork. We build every case as if it's going to trial from day one. That means collecting police reports, deposing witnesses, and hiring accident reconstructionists and medical experts to build an undeniable case for the full value of your damages.

This level of preparation sends a clear signal: we won't be backing down. It's the credible threat of trial that forces insurers to stop playing games and start negotiating in good faith. Suddenly, those lowball offers disappear, and realistic numbers appear on the table.

Best of all, you don't pay us a dime to get started. We work on a contingency fee basis, which means we only get paid if we win money for you. If we don’t recover compensation, you owe us nothing. It's that simple.

Common Questions About Car Accidents And Medical Bills

When you’re hurt, the last thing you want to worry about is a mountain of medical bills and confusing legal deadlines. It’s stressful, and it’s completely normal to have questions. We hear them all the time from clients in Pennsylvania and New Jersey. Here are some straightforward answers to the questions we get asked the most.

What If The Other Driver Was Uninsured Or Fled The Scene?

This is a true nightmare scenario. But it’s exactly why your own Uninsured/Underinsured Motorist (UM/UIM) coverage exists. This part of your policy is your lifeline when the at-fault driver has no insurance or takes off after the crash.

Your insurance company essentially steps into the shoes of the person who hit you. They become responsible for your medical bills, lost wages, and pain and suffering, right up to your policy limits.

But here’s the catch: even though it's your insurance company, they won't just hand over a check. They will still fight to pay out as little as possible. It can feel surprisingly hostile. Having an experienced attorney is critical to make sure you get the full benefits you’ve been paying for.

How Long Do I Have To File A Car Accident Lawsuit?

Every state has a strict time limit to file a personal injury lawsuit. It’s called the statute of limitations, and if you miss it, your right to sue is gone forever.

In both Pennsylvania and New Jersey, the statute of limitations for a car accident injury claim is two years from the date of the accident.

There are almost no exceptions. This is why you need to talk to a lawyer long before that two-year clock runs out. It gives us the time we need to investigate your case, gather all the evidence, and build the strongest claim possible. Don't wait until the last minute.

Do I Really Have To Go To Court?

This is probably the biggest fear we hear. The idea of a courtroom battle is intimidating for anyone.

The good news? The vast majority of our cases—over 95%—settle without ever going to trial.

The secret to a great settlement is making the insurance company believe you’re ready, willing, and able to take them to court and win. We prepare every single case for trial from day one. This lets us negotiate from a position of power and often convinces the insurer to offer a fair deal to avoid the risk and expense of a jury verdict. And if they won’t be reasonable? We are always ready to fight for you in court.

Every car accident is different, and the answers to your questions will depend on the unique facts of your case. For clear, personalized guidance on your accident and medical bills, the trial lawyers at Mattiacci Law are here to help. Contact us for a free consultation and get the answers you need.