Author: John Mattiacci | Owner Mattiacci Law

Published May 21, 2026

A crash claim can lose value before the first settlement call, because of a box checked on an auto policy.

Full tort insurance preserves your right to pursue the full range of damages against the at-fault driver, including pain and suffering. Limited tort trades away part of that right for a lower premium. On paper, that can look like a routine insurance choice. In an injury case, it affects what the insurer has to fear, what your lawyer can demand, and how much pressure exists to settle fairly.

I see the problem after collisions, not at renewal time. A Philadelphia driver gets hurt, follows medical advice, misses work, and expects the insurance process to reflect what the injury has done to daily life. Then the carrier points to a limited tort election and tries to treat the case like a reimbursement file instead of a human loss case.

That shift matters. Full tort often gives a claim more settlement value because the defense has to account for the injury itself, not just medical bills and wage records. It also changes litigation strategy. A case with unrestricted noneconomic damages presents a different risk to the insurer, and insurers evaluate risk in dollars.

Many drivers never get a real explanation when they buy coverage. They are comparing premiums, trying to get through the paperwork, and dealing with normal life. After a wreck, they are also trying to find treatment and recover, sometimes looking for providers such as LifeWorks Integrative Health for accident injuries.

The question is not just what full tort means in theory. The real question is what your tort election does to the value of your case, your bargaining position, and your options if the insurer refuses to be reasonable.

The Insurance Choice That Can Define Your Recovery

A driver gets rear-ended on I-95. At first, the case looks straightforward. The other driver was careless. The medical treatment starts. The injured person misses work, struggles to sleep, and can't lift their child without pain.

Then the insurance policy comes out.

If that driver chose limited tort, the conversation changes fast. The insurer may still have to deal with the economic losses, but the claim for pain and suffering may be restricted unless an exception applies or the injury qualifies as legally serious. If the driver chose full tort, the claim starts from a different place. The insurer has to account for the human harm, not just the invoices.

That difference isn't abstract. It affects how lawyers evaluate the file, how adjusters set reserves, and whether settlement talks begin with real pressure or with a built-in ceiling.

Why clients get blindsided

People usually don't call a lawyer asking about tort elections. They call because they're hurt and confused. They're trying to manage treatment, car repairs, lost income, and paperwork all at once. Many are also searching for practical care options, including resources like LifeWorks Integrative Health for accident injuries, while they sort out the legal side.

The insurance form feels minor when you buy the policy. After a collision, it can become one of the most important documents in the case.

In Pennsylvania and New Jersey, this choice deserves more attention than it gets. A lower premium can sound appealing when nothing is wrong. After a real injury, the legal limits can feel very different.

What this choice really controls

At bottom, tort selection controls one major question. Do you keep full access to the value of an injury case, or do you trade part of that access for cheaper premiums?

That is why lawyers pay close attention to it early. If the policy preserves broad recovery rights, the case strategy expands. If it doesn't, the first task is often figuring out whether an exception restores those rights.

Understanding Full Tort The Unrestricted Right to Recover

A client comes into my office after a rear-end crash with real injuries. The MRI shows a disc problem. Physical therapy drags on for months. Work becomes harder. Sleep gets worse. One of the first questions I ask is simple. Did you choose full tort or limited tort?

That answer can shape the value of the case from day one.

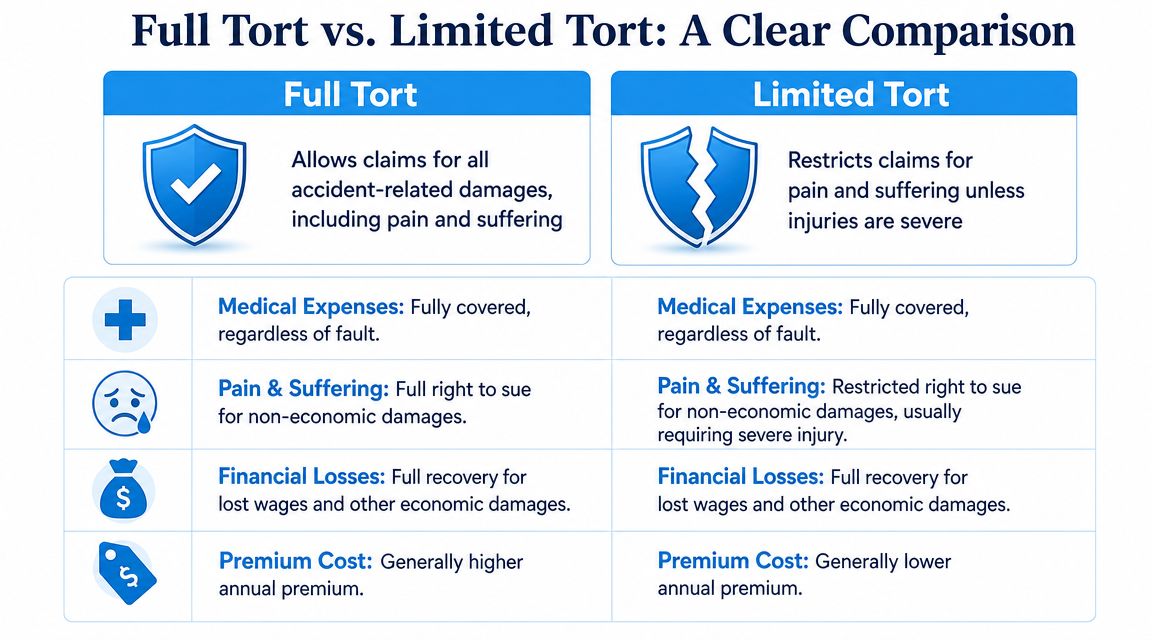

Full tort preserves your right to pursue the full range of damages Pennsylvania law allows after a car accident. You still have to prove the other driver was at fault. You still have to prove the crash caused your injuries. You still need medical evidence and a clear damages story. But your own policy election does not block a pain-and-suffering claim the way a limited tort insurance election can.

From a trial lawyer's standpoint, that matters because injury cases are not valued on medical bills alone. Actual harm often shows up in the parts of life that do not come with receipts. Missed family activities. A job done through pain. Interrupted sleep. The loss of a normal routine.

What unrestricted means in a real case

With full tort, the claim can include economic losses and non-economic harm.

That usually means compensation for:

- Medical expenses: ER care, imaging, follow-up visits, physical therapy, prescriptions, and future treatment tied to the crash

- Lost income: Wages, missed work opportunities, and reduced earning ability if the injury affects your job

- Property loss: Vehicle damage and related out-of-pocket costs

- Pain and suffering: Physical pain, limitations, inconvenience, and the way the injury changes daily life

Pain and suffering is often the turning point. Insurance companies know that. If a case includes only bills and wage loss, the discussion is narrower. If the case also includes credible human damages, the exposure is broader, and the defense has to evaluate the claim differently.

Why full tort changes case strategy

Full tort gives your lawyer room to present the whole injury, not just the invoice stack. That affects witness preparation, medical record review, settlement posture, and trial value. It also changes how an adjuster reserves the file because the insurer has to account for non-economic damages rather than treating the case like a reimbursement exercise.

I have seen cases where the biggest loss was not the ambulance bill. It was the client's inability to sit through a shift, pick up a child, drive without pain, or return to the routines that made life normal. Full tort keeps those losses in play.

For firms focused on documenting damages clearly and presenting them effectively, systems aimed at improving settlement outcomes for legal teams can help organize treatment records, timelines, and symptom evidence. The starting point, though, is still the legal right preserved by the policy.

Practical rule: Full tort does not promise a large settlement. It preserves the right to demand payment for the full harm the crash caused.

Clients sometimes confuse full tort with full coverage. They are different choices. Full coverage usually refers to the types of insurance on the vehicle. Full tort is about your legal right to recover for all categories of injury damages if another driver hurts you.

Full Tort vs Limited Tort A Side-by-Side Comparison

This comparison isn't "good policy" versus "bad policy." It's lower cost now versus broader legal rights later. That trade-off deserves a plain-English look.

The clearest differences

| Issue | Full tort | Limited tort |

|---|---|---|

| Upfront cost | Usually higher premium | Usually lower premium |

| Pain and suffering claim | Broadly preserved | Restricted unless threshold or exception applies |

| Claim posture | Insurer must account for economic and non-economic exposure | Insurer may focus on economic loss only |

| Settlement leverage | Generally stronger because more damages are in play | Often narrower unless limited-tort barriers are overcome |

| Best fit | Drivers who want to preserve full legal rights | Drivers prioritizing short-term premium savings |

Some Pennsylvania firms note that limited-tort policies are often only about $100 to $200 cheaper per year than full-tort policies, which is a relatively small annual savings compared with the potentially much larger recovery difference in a catastrophic injury case (annual premium difference often cited in Pennsylvania).

What the cheaper option really buys you

Limited tort is not worthless coverage. It can still allow recovery for medical bills, wage loss, and property damage. For some people, that lower premium feels like a practical compromise.

But here's the problem. Many collisions produce injuries that are painful, disruptive, and expensive without fitting neatly into a threshold fight the insurer is happy to concede. That's where limited tort can turn into a claims obstacle rather than a savings strategy.

If you want a deeper look at the restricted option itself, this explanation of limited tort insurance in Pennsylvania is a useful companion.

The comparison lawyers make

From the plaintiff side, the question is simple. Which policy leaves the fewest openings for the defense?

- Full tort reduces one major defense theme: The insurer can't rely on your own election to wall off non-economic damages.

- Limited tort creates an extra fight: Before negotiating full value, you may need to prove a threshold issue or fit within an exception.

- Serious cases expose the gap: The worse the life impact, the more painful it is to discover the policy restricted the claim.

A cheaper policy can save money during a quiet year. It can cost much more when a real injury changes your routine, work, and family life.

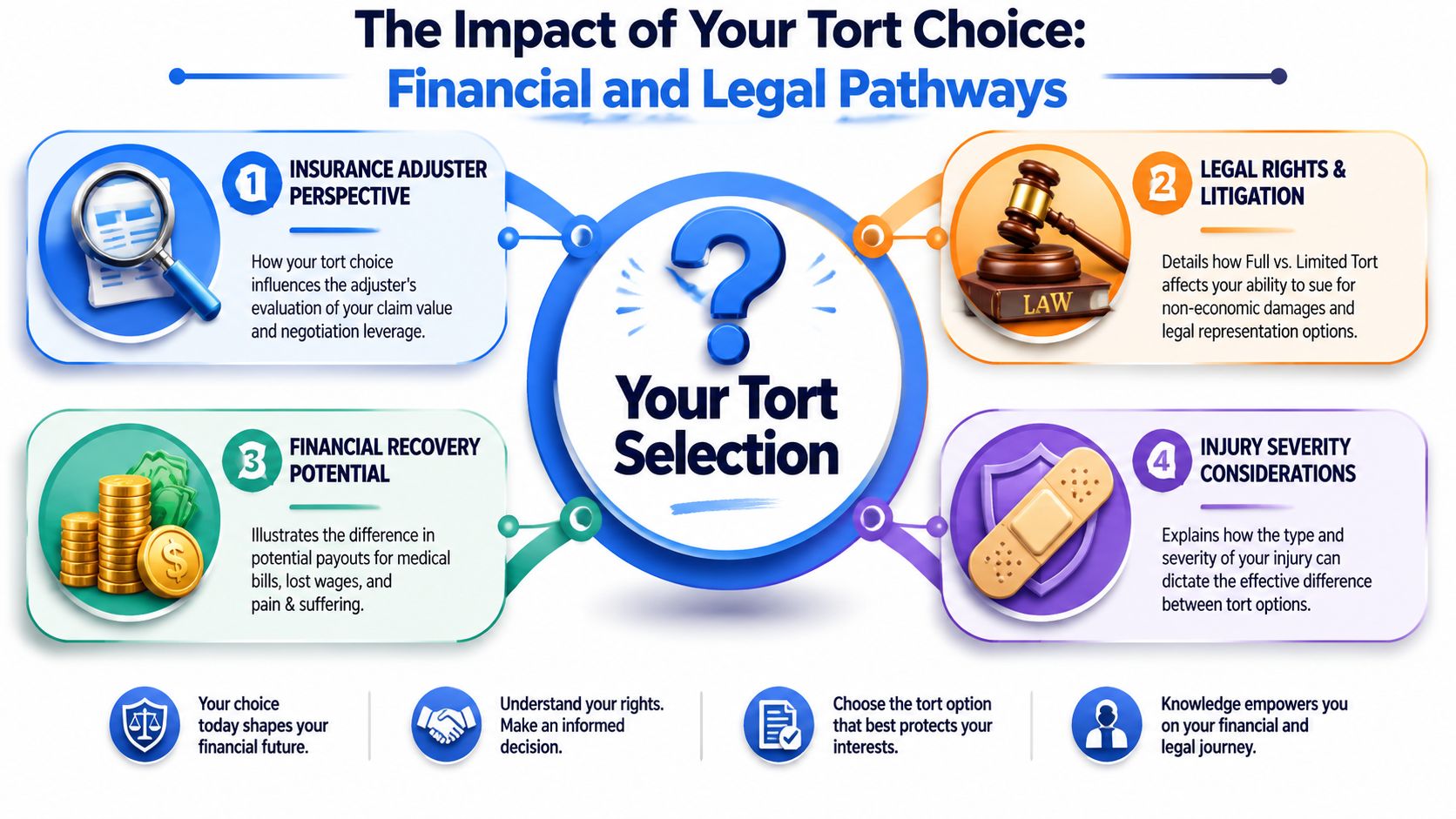

The Financial and Legal Impact of Your Tort Selection

A crash victim can walk into my office with clear medical treatment, missed work, and months of pain, yet the value of the claim may still turn on a box checked on an insurance form years earlier. That is the practical impact of tort selection.

The first question on the defense side is simple. What damages are available? Full tort usually keeps the full case on the table from the start, including medical bills, lost income, vehicle damage, and pain and suffering. Limited tort can shrink that discussion early and force a separate fight over whether the injury clears the legal threshold. As one Pennsylvania injury firm explains, full tort often affects case value because the claim is not restricted to out-of-pocket losses alone (how full tort affects valuation and claim value).

How tort choice affects settlement negotiations

Insurance carriers do not pay claims in the abstract. They price risk. If the jury may hear how an injury changed sleep, parenting, work stamina, exercise, driving, or basic daily comfort, the insurer has more to account for during negotiations.

That changes the tone of the case.

In a full-tort claim, the damages story starts with the records but does not end there. The claim is built around the actual effect of the injury on the person's life. In a limited-tort claim, the defense often tries to keep the case confined to bills, wage records, and property damage unless the injured person can prove an exception or serious impairment.

What changes in the evidence

The evidence shifts with the rights available under the policy. If pain and suffering is part of the case, the proof has to show more than a treatment timeline.

Strong case files usually focus on:

- Medical causation: Records that tie the crash to the diagnosis, complaints, and course of care.

- Functional loss: Evidence of work restrictions, missed tasks, reduced mobility, and trouble with normal routines.

- Duration and consistency: Documentation showing the symptoms continued and were reported consistently over time.

- Human impact: Testimony and records that show what the injury changed in daily life.

The best injury cases answer one question clearly. What did this crash cost the person beyond the invoices?

That is why lawyers push clients to keep appointments, report symptoms accurately, and avoid gaps in care that create doubt. Full tort gives counsel room to present the full picture. It does not remove the need to prove it well.

How defense strategy shifts

Defense lawyers look for limits they can use. Limited tort gives them one more argument at the policy level. If they can keep pain and suffering out of the case, they may be able to reduce the claim's settlement range before the medical proof is even fully developed.

Full tort takes that argument away. The defense can still dispute fault, challenge causation, point to prior injuries, or argue the treatment was excessive. But they cannot rely on your own tort election to block non-economic damages from the outset.

That difference also affects how a serious case is prepared. Lawyers may need treating doctors, expert review, wage documentation, and testimony from the people who see the client's daily limitations firsthand. This is the kind of detailed case development firms like Mattiacci Law handle in Pennsylvania and New Jersey when the value and posture of the case depend in part on the policy election.

Why this matters after the crash, not just before it

After the collision, the tort election is no longer a budgeting decision. It becomes a case-value issue.

If the policy is limited tort, the job is to examine the policy language, the injury evidence, and any exception that may allow a broader recovery. If the policy is full tort, the job is to document the losses in a way that makes the insurer take the claim seriously.

Insurance companies rarely point out every path that may expand a claim. Someone has to find those paths, prove them, and press the case accordingly.

Is Full Tort Worth the Higher Premium

For most drivers, I view this as a risk-allocation decision, not a line-item budgeting exercise. The premium difference matters. But so does the size of the right you're giving up.

Bankrate notes that full tort broadens the ability to sue for medical and non-monetary damages, while limited tort usually restricts pain-and-suffering claims unless an injury is serious. It also highlights the common consumer problem: people hear that limited tort is cheaper, but they don't get a clear answer on the financial value of preserving full tort rights (Bankrate overview of tort insurance trade-offs).

The practical cost-benefit test

If you are choosing coverage before any accident happens, ask yourself three things:

How much risk are you comfortable carrying?

Limited tort saves money up front. In return, you accept the risk that a meaningful injury claim may be legally narrowed.What would happen if your injury disrupted work or home life?

Many people focus on hospital bills and forget how much suffering, inconvenience, and functional loss shape a real injury claim.Would the premium savings feel worthwhile after a difficult recovery?

That answer often changes once people think past minor fender-benders and consider months of pain, treatment, or reduced mobility.

When full tort makes the most sense

Full tort is often the better fit for:

- Daily drivers: More time on the road means more exposure.

- People with physical jobs: Missing work or working in pain can change the value of a claim quickly.

- Parents and caregivers: Injury affects more than employment. It affects home life.

- Anyone who wants fewer legal obstacles: Full tort removes one major restriction before a claim even starts.

Paying more for full tort isn't buying a bigger insurance card. It's buying back legal options that can matter a great deal after a serious injury.

When people still choose limited tort

Some drivers choose limited tort because the lower premium fits their budget, and that is a real consideration. Others assume severe cases will always clear the threshold anyway.

That assumption is where problems start. Borderline cases create disputes. The injury can be very real, very disruptive, and still become a fight over whether non-economic damages are available. Full tort avoids that fight at the front end.

Common Questions About Pennsylvania Tort Insurance

A lot of bad claim decisions start with one wrong assumption. Someone sees "limited tort" on the declarations page and concludes the case has little value. Sometimes that is true. Sometimes it is not, and the difference can mean whether an insurer treats the claim as a nuisance file or a serious exposure.

What if I chose limited tort but an exception applies

Then the analysis changes fast.

The exception question matters because it can reopen a claim for pain and suffering that looked restricted at first. From a litigation standpoint, that affects how the case is investigated, how damages are documented, and how the insurer evaluates risk.

Here is where the details matter:

- Commercial vehicle collisions: If the other vehicle was being used in business, the law may treat the limited-tort election differently. That issue comes up in delivery van crashes, company truck wrecks, contractor vehicle collisions, and some employer-use situations. The reason it matters is practical. Commercial cases often involve larger policies, business records, and defendants who fight early over scope of employment and coverage.

- Uninsured at-fault drivers: A driver who should have had coverage but did not can change the tort analysis. That can also shift attention to your own uninsured motorist coverage and how the claim should be presented under that policy.

- Intentional conduct: Road rage, deliberate assault with a vehicle, or other intentional wrongdoing can move the case outside the ordinary limited-tort framework. Those facts need to be pinned down early through the police report, witness statements, and any available video.

I have seen people leave real money on the table because nobody examined the exception issue closely enough. The label on the policy is only the starting point.

Does Pennsylvania being a no-fault state make tort choice irrelevant

No. The two concepts do different jobs.

Pennsylvania no-fault rules govern first-party medical benefits under your own policy. Tort selection affects what you may pursue against the driver who caused the crash, especially for pain, suffering, and loss of life's normal activities. If you want a clearer explanation of how those systems work together, this guide to Pennsylvania's no-fault car insurance rules lays out the basics.

What about passengers, rideshares, and work vehicles

These cases create confusion because the injured person is not always the one who chose the policy terms.

A passenger may have rights that do not match the driver's assumptions. A rideshare crash can involve the driver's personal policy, the rideshare company's coverage, and disputes about whether the app was on. A work-vehicle case can raise questions about commercial use, employer policies, and whether the driver was acting within the scope of the job when the crash happened.

Rental cars and multi-vehicle crashes add another layer. There may be several policies, several defendants, and several arguments about which tort election controls. That is why these cases should be reviewed early, before the insurer reduces the claim to a single box on a form.

"Limited tort" does not answer every coverage question. In the right factual setting, the crash itself can change what damages are available.

If I'm already hurt, what should I do first

Get the policy documents. Get the crash report. Keep your treatment records, wage-loss information, and photos that show how the injury has affected daily life.

Then have a lawyer review the tort election alongside the facts of the crash. That review should happen before you give the insurer room to define the injury as minor, temporary, or legally restricted when the file may support much more.

Don't Let an Insurance Form Limit Your Future

Full tort is one of the few insurance choices that directly affects both the value of an injury case and the pressure an insurer feels to resolve it fairly. That is why this election matters so much. It doesn't just shape what you pay for coverage. It shapes what rights survive after someone else causes harm.

If you're choosing coverage now, think beyond the premium difference. Ask what happens if the injury isn't minor, if the recovery drags on, or if the losses can't be captured by bills alone. Full tort preserves room to pursue the claim as a whole.

If you've already been injured, don't guess about what your policy means. A limited-tort election may still involve exceptions, and a full-tort election changes how the case should be presented from the start. Waiting too long can let the insurer define the narrative before your side has built the evidence.

People in the Philadelphia area often come to these questions at the worst time. They're hurt, missing work, and trying to make sense of unfamiliar terms while adjusters ask for statements and records. That is exactly when clear legal advice matters most.

If you're unsure whether it's time to bring in counsel, this overview on when to hire a personal injury lawyer can help you think through the timing.

If a crash has left you wondering how your tort election affects your claim, talk with Mattiacci Law. The firm represents injured people in Pennsylvania and New Jersey, reviews policy elections and exceptions, and evaluates how those issues affect settlement value, litigation strategy, and the ability to recover full compensation.

Frequently Asked Questions

Is full tort better than limited tort?

How much more does full tort insurance cost?

Can you sue for pain and suffering with full tort insurance?

What happens if you choose limited tort instead of full tort?

Does full tort insurance cover medical bills?

Is full tort required in Pennsylvania?

What are the exceptions to limited tort in Pennsylvania?

Serious injuries

Drunk driving accidents

Out-of-state vehicles

Commercial vehicle crashes

Pedestrian accidents

Motorcycle accidents