Author: John Mattiacci | Owner Mattiacci Law

Published April 8, 2026

You were driving home, or heading to a job site, or taking your child to school. Another driver caused the crash. You reported it. You got medical care. You expected their insurance company to do what it is supposed to do.

Then the denial came.

Sometimes it is direct. “We are denying liability.” Sometimes it is dressed up as delay. They say they need more time, more records, another statement, another review. Sometimes they make an offer so low it functions like a denial.

That moment rattles people because it feels final. It is not. In Pennsylvania, a denial is often the start of the fight.

When people search for What Happens If The At Fault Driver’s Insurance Won’t Pay In Pennsylvania, they want a straight answer, not insurance jargon. The straight answer is this: you may still have several paths to recover compensation, but the path that works best depends on why the insurer refused to pay and how quickly you start building pressure against them.

A weak claim gets ignored. A trial-ready claim gets attention.

The Insurance Company Said No Now What

A common scenario looks like this. The other driver rear-ends you at a light. The police respond. The report seems favorable. Your car is damaged, your back and neck hurt, and your treatment starts within days. Then the adjuster calls and says they are “still investigating,” or worse, they deny the claim because liability is “unclear.”

That feels absurd, especially when the crash seemed obvious.

It also happens more often than people expect. Insurance companies do not treat a denial as a moral judgment. They treat it as a position in a negotiation. If you accept it, they save money. If you push back with evidence and legal advantage, the position can change.

For injured people, the first mistake is assuming the denial letter is the end. The second mistake is arguing with the adjuster without a strategy. What matters is not outrage. What matters is building proof, preserving options under your own policy, and preparing the case as if a lawsuit may be necessary.

A denied claim can still turn into payment through a renewed liability claim, a UM or UIM claim, litigation against the driver, or in the right case, a bad faith action against the insurer. Each option has a different purpose. Each requires a different kind of pressure.

If your situation sounds familiar, this overview of someone hit my car and the insurance company denied my claim is a useful starting point. The key is not to drift while bills, records, and deadlines pile up.

A denial is a tactic until a judge or jury says otherwise. Treat it like a position to challenge, not a verdict to accept.

Why Pennsylvania Insurers Deny At-Fault Accident Claims

Most denial letters sound technical. The underlying reasons are practical. The insurer wants a basis, or at least a talking point, to avoid paying full value.

They dispute fault because shared blame saves them money

Pennsylvania follows modified comparative negligence. If the injured person is found to be more than 50% at fault, recovery is barred. If the injured person is under that threshold, compensation is reduced by that share of fault. For example, 30% fault cuts compensation by 30% according to Wilk Law Firm’s discussion of proving liability in Pennsylvania car accident claims.

That rule gives insurers a playbook.

They look for anything they can frame as your mistake: speeding, distraction, following distance, lane position, even inconsistent wording in your recorded statement. In a cleaner case, they may argue partial fault to reduce value. In a harder case, they push the blame argument far enough to try to shut the claim down entirely.

This is why early evidence matters. Once the insurer hardens around a fault defense, every missing photo, every unwritten witness recollection, and every vague medical record makes their position easier to maintain.

They rely on exclusions hidden inside the policy

Sometimes the carrier is not saying the crash did not happen. They are saying the policy does not apply.

That shows up in several forms:

- Business-use exclusion: The driver was delivering, ridesharing, or otherwise working when the crash happened.

- Lapsed or canceled coverage: The policy was not active.

- Unlisted driver or ownership issue: The person behind the wheel may not fit within the coverage terms.

- Intentional conduct or other policy defenses: The insurer claims the event falls outside what the contract covers.

These denials can be harder than ordinary fault disputes because you are no longer arguing only about how the crash occurred. You are also fighting over policy language.

They attack gaps in treatment and documentation

Insurers know juries pay attention to timing. So do adjusters.

If you waited to get checked, missed appointments, changed providers repeatedly, or underreported symptoms early and reported more serious problems later, the insurer may argue that your injuries are minor, unrelated, or exaggerated. The same goes for property damage documentation, wage loss proof, and any silence in the record about how the injuries changed your daily life.

A denial often grows out of these small record gaps, not one dramatic issue.

They stall because delay itself creates pressure

Some denials are not final in practice. They are part of a pressure campaign.

The insurer knows that claimants often need car repairs, income, and treatment support now, not after months of letters and document requests. Delay can push people into taking a weak offer to get movement.

When an insurer asks for “just one more thing,” ask whether the request is legitimate, whether you already provided it, and whether the delay is serving a real investigation or a bargaining strategy.

What is effective against these tactics

Strong claims are organized before the insurer asks for proof.

That means liability evidence, scene photos, witness names, vehicle damage images, medical records tied tightly to the crash, and a clear damages package. It also means knowing when not to keep explaining yourself to an adjuster who is collecting statements to use against you later.

The denial reason matters, but the strategic response matters more. If they are arguing fault, you need proof. If they are citing a policy exclusion, you need the policy. If they are minimizing injury, you need a disciplined medical and damages record.

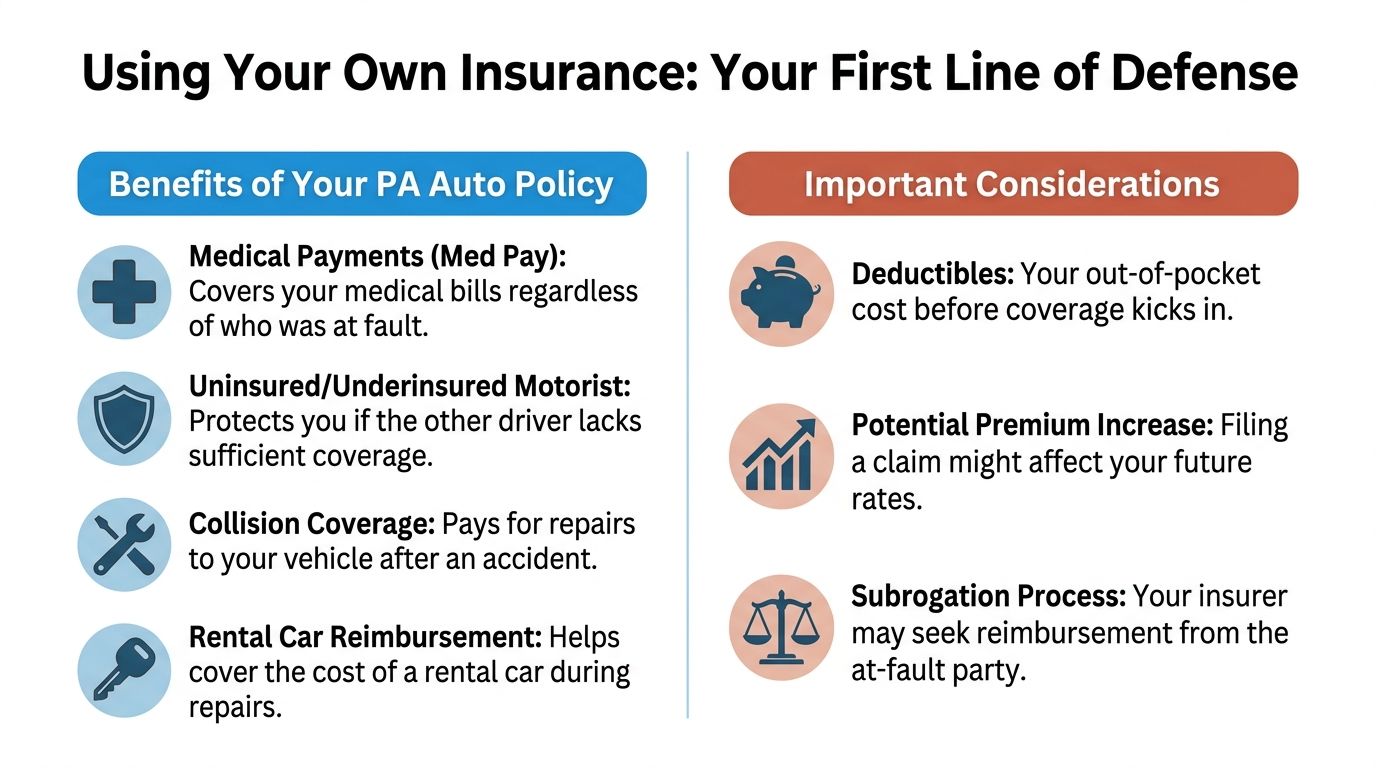

Using Your Own Insurance Your First Line of Defense

When the at-fault driver’s carrier refuses to act reasonably, your own policy becomes the practical starting point. In Pennsylvania, that is not a sign of weakness. It is how many claims stay afloat while the liability fight unfolds.

Start with what your policy pays now

Pennsylvania requires minimum liability coverage of $15,000 per person for bodily injury, and all drivers must also carry at least $5,000 in Personal Injury Protection. That PIP benefit is often exhausted quickly in a serious injury case, which is why third-party claims become necessary, as explained by Reiff Law Firm’s Pennsylvania uninsured and underinsured driver overview.

The practical use of your own policy breaks down like this:

- PIP: Pays initial medical benefits regardless of fault.

- Collision coverage: Can address vehicle repairs faster than waiting for the other carrier to accept liability.

- Rental reimbursement: Helps keep you moving if your policy includes it.

- UM or UIM coverage: Often becomes the most important protection when the other side has no coverage, denies coverage, or carries too little coverage.

People resist opening a claim under their own policy because they think it means surrendering the argument against the other driver. It does not. It means using the tools you already paid for.

If your damage includes glass or visibility issues that need immediate repair, a practical question is whether insurance covers broken car windows. Property damage delays can create safety problems long before the liability case resolves.

UM and UIM are often the difference between a dead end and a viable claim

Uninsured Motorist coverage can apply when the at-fault driver has no collectible insurance for your loss. Underinsured Motorist coverage can apply when the available liability limits are too small for the harm done.

From a trial lawyer’s perspective, these claims require the same discipline as a lawsuit against the other driver. Your own insurer is not acting as your friend just because you have a policy with them. In a UM or UIM claim, your insurer often evaluates the case like an opposing carrier.

That means you still need proof of fault, proof of injury, and proof of damages.

Limited Tort and Full Tort change what pressure you can apply

Pennsylvania’s tort election matters because it affects whether you can pursue pain and suffering in an ordinary case.

Here is the cleanest comparison:

| Feature | Limited Tort | Full Tort |

|---|---|---|

| Right to seek pain and suffering | Restricted unless an exception applies | Broadly preserved |

| Cost of coverage | Usually cheaper | Usually more expensive |

| Lawsuit flexibility | Narrower | Wider |

| Strategic advantage in injury claim | More constrained | Stronger |

If you chose Limited Tort, the case can still be valuable, but the insurer knows your non-economic damages claim may be restricted unless an exception applies. If you chose Full Tort, the insurer faces broader exposure from the start.

This is one reason policy review happens early in serious cases. You cannot build influence if you do not know what rights your own policy preserved.

Use your own coverage deliberately

Do not treat your policy like a backup folder you check at the end. Treat it like part of the litigation plan.

A disciplined approach looks like this:

- Open the available first-party claims promptly. That preserves access to benefits while the liability dispute continues.

- Request the full declarations page and endorsements. You need to know what coverages exist, not what you assume exists.

- Keep every payment record. Your own carrier’s payments can become important later in reimbursement and case valuation.

- Coordinate the property damage side and injury side separately. They often move on different timelines.

Your own insurance can buy time, treatment access, and repair options. It does not replace the claim against the at-fault side, but it can prevent the denial from boxing you in financially.

Building Your Case How to Prove Fault and Damages

A denied claim means one thing: the insurer believes your proof is weak, incomplete, or vulnerable to attack. The response is not more argument. The response is better evidence.

Build the liability file first

Start with the crash itself. A strong liability file should answer a simple question: why is the other driver legally responsible?

That file includes:

- Police report: Not final proof by itself, but an important anchor.

- Scene photographs: Road layout, debris, skid marks, signals, weather, and vehicle positions.

- Vehicle damage photos: Taken before repairs if possible.

- Witness information: Names, numbers, and what each witness observed.

- Video sources: Dashcams, nearby businesses, home cameras, and intersection footage.

- Your own statement: Kept accurate, concise, and consistent.

If the other driver was working for a service like Uber or a delivery company, the denial may be based on a business-use exclusion in the personal policy. Challenging that often requires obtaining the full policy and examining whether the exclusion applies, as noted by Swoper and Pell’s discussion of what to do if the at-fault driver’s insurance will not pay.

That single issue can change the whole case. Now you may be looking at the driver’s personal insurer, a commercial policy, the company relationship, app status, and policy language all at once.

Prove damages with the same care

Insurers deny injury cases on liability grounds, but they also deny them by shrinking the damages picture.

Your damages proof should include more than bills.

Medical proof

Collect every record from the first visit forward. That includes emergency care, imaging, specialist visits, therapy notes, prescriptions, and discharge instructions. Consistency matters. So does showing that your symptoms continued over time instead of appearing only when settlement discussions started.

If your doctor recommends rehabilitation, information on Auto Accident Physical Therapy can help you understand the role treatment records play in both recovery and case documentation.

Income loss proof

This means pay stubs, tax records, employer letters, and documentation of missed work or reduced duties. If you are self-employed, the proof often requires more careful assembly because the insurer will challenge anything that looks estimated rather than documented.

Human damages

Pain, limitations, sleep disruption, missed family activities, and loss of normal function are real damages, but they are easy to understate if no one records them properly.

A simple journal can help. Not a dramatic diary. Just clean entries about symptoms, restrictions, appointments, and what you could not do that day.

Juries and adjusters both trust records made close in time to the events. A well-kept journal is often more persuasive than a polished explanation given much later.

Organize the file like you are handing it to a jury

Sloppy claims invite denial. Trial-ready claims force decisions.

That means creating one coherent file, not a pile of disconnected documents. Dates should line up. Treatment should track the injury story. Photos should be labeled. Wage loss should tie to records. If there is a gap, address it directly instead of hoping the insurer overlooks it.

For a closer look at how lawyers assemble and use proof, this page on how evidence is used to prove negligence in Pennsylvania is useful.

What does not work

People often hurt their own case in predictable ways:

- Giving repeated recorded statements after the insurer has already signaled hostility.

- Posting casually online about activity levels, travel, or work.

- Treating only when symptoms spike and leaving long undocumented gaps.

- Sending unorganized records and expecting the adjuster to connect the dots fairly.

Insurance companies do not build your case for you. They inspect it for cracks.

Taking Legal Action Suing the Driver and Their Insurer

When the insurer refuses to move, filing suit changes the power dynamic. A claim is a request. A lawsuit is a demand backed by court rules, deadlines, discovery obligations, and the risk of trial.

Suing the driver is often how you force the insurer to engage

In most Pennsylvania car crash cases, the immediate lawsuit target is the at-fault driver, not the insurer. That matters because the driver’s carrier typically has a duty to defend its insured if the claim falls within coverage.

Once suit is filed, the insurer cannot just hide behind casual phone calls and form letters. Defense counsel appears. Written discovery starts. Testimony can be compelled. Positions that sounded easy in a denial letter become harder to maintain under oath.

This is one reason trial lawyers prepare from day one. The facts that win a lawsuit often create the advantage that settles it before trial.

Suing the driver personally has limits, but sometimes it matters

Clients often ask whether it is worth suing the individual driver if insurance coverage is thin, denied, or exhausted.

Sometimes yes. Sometimes no.

The practical issue is collectability. A judgment against an individual is only as useful as the assets available to satisfy it. In many cases, pursuing a personal judgment has limited value. In others, especially when there are business interests, non-exempt assets, or additional responsible parties, it can matter a great deal.

That decision should be strategic, not emotional.

Bad faith changes the exposure

Pennsylvania gives injured parties and insureds an important tool when an insurer denies or handles a claim without a reasonable basis. Under 42 Pa.C.S. §8371, a court can award interest, punitive damages, and attorney’s fees on top of the underlying claim when bad faith is proven, as described in this explanation of what happens when someone hits your car and their insurance will not pay.

That is a powerful advantage.

A bad faith theory may come into play when the insurer ignores clear liability evidence, refuses to evaluate the claim with integrity, relies on pretext instead of a thorough investigation, or delays without a reasonable basis. The details matter. So does timing. Not every denial is bad faith. But some are.

The strongest strategy often uses both tracks

Here, people misunderstand the legal fight. They think they must choose one road.

In serious cases, influence often comes from using multiple pressure points at once:

- The liability lawsuit against the driver forces formal litigation.

- Coverage investigation tests whether an exclusion or denial is valid.

- UM or UIM pursuit preserves first-party recovery options if available.

- Bad faith analysis raises the stakes if the insurer’s conduct crossed the line.

Each track affects the others. A weak insurer position on liability can become more obvious in discovery. A shaky exclusion defense may collapse once the policy and underlying facts are scrutinized. A carrier that thought it was controlling costs may suddenly face risk beyond the original claim value.

The goal is not to file everything possible. The goal is to identify which legal tools create significant pressure in your specific case and use them in the right order.

Litigation discipline matters early

Filing suit without a record is not strategy. It is noise.

Before filing, a lawyer should know the liability theory, the injury theory, the policy issues, the likely defenses, and what documents or testimony will be needed first. That is how you avoid chasing the case after litigation begins.

A serious claim should enter court already organized around proof. That is what makes negotiation credible later.

Navigating the Legal Process Negotiation vs Litigation

Many people have never been through a lawsuit. They imagine either a quick settlement or a dramatic trial. Typically, there is a long middle period where preparation drives outcome.

A typical Pennsylvania case starts with a demand or renewed claim effort. If the insurer stays unreasonable, suit is filed. Then the case enters formal litigation, where each side has to produce information instead of just making assertions.

What negotiation looks like when it has real force

Good negotiation is not repeated phone calls asking the adjuster to reconsider. Good negotiation is presenting a case the other side believes can beat them later.

That means the file is already built. Medical records are organized. Liability proof is lined up. Wage loss is documented. The insurer understands that if it keeps denying or discounting the claim, the next step is not another pleading email. It is discovery, depositions, and trial preparation.

When the other side believes you are bluffing, negotiation stalls. When they believe you are ready, talks often change tone.

What litigation entails

Once a lawsuit is filed, several things usually happen.

First comes written discovery. Each side sends questions and document requests. At this stage, the defense has to commit to positions on fault, injuries, and defenses.

Then come depositions. A deposition is sworn testimony taken before trial. The injured person may be questioned by the defense lawyer. The at-fault driver can also be questioned. Witnesses, treating providers, and other relevant people may become part of the process too.

The point is simple. Discovery turns vague denials into testable positions.

Why the case may still settle after suit is filed

Filing a lawsuit does not mean trial is guaranteed. It often means a thorough evaluation begins.

Insurers frequently pay closer attention once defense counsel reports back on witness credibility, document quality, medical support, and how the plaintiff would likely present to a jury. A case prepared for trial often resolves before trial because the preparation itself exposes the risk.

That is why trial-focused firms build early. The work is not wasted if the case settles. The work is what provides the settlement value.

Where Assigned Claims fits if other options fail

Some cases are unusually difficult because no usable insurance is available. In that narrow corner, Pennsylvania’s Assigned Claims Plan can provide up to $15,000 in medical benefits, but it does not cover pain and suffering or property damage, as outlined by Munley Law’s explanation of no-insurance situations when the other driver was at fault.

That makes it a limited safety net, not a full solution.

If Assigned Claims is even part of the conversation, the rest of the strategy should be examined carefully. There may still be a UM claim, a disputed coverage issue worth challenging, or a personal liability route worth evaluating.

What clients should expect

The legal process can take time. That is not pleasant, but it is honest.

What matters is whether each month is producing something useful: records, testimony, admissions, policy documents, expert support, or negotiation pressure. Delay with a plan is different from drift. A good litigation strategy keeps the case moving toward proof and advantage, even when resolution is not immediate.

Why You Need a Pennsylvania Trial Attorney on Your Side

There is a point where this stops being an insurance claim and becomes a legal contest. That point arrives when fault is disputed, coverage is denied, injuries are significant, or the insurer starts using your own words and records against you.

At that stage, representation matters because advantage matters.

A Pennsylvania trial attorney does more than “handle the paperwork.” The actual work is harder and more specific. It involves identifying every available coverage path, locking down evidence before it disappears, protecting the client from statement traps, organizing medical proof, and pushing the case into litigation posture early enough that the insurer takes the threat seriously.

That is especially important when the case includes any of these problems:

- Disputed liability

- Serious injury or future treatment needs

- Limited Tort complications

- Business-use or other coverage exclusions

- UM or UIM disputes with your own carrier

- Conduct that may support a bad faith claim

In those cases, the difference between an adjuster-level claim and a trial-ready claim is often the difference between frustration and meaningful recovery.

A lawyer also brings discipline to decision-making. Not every case should be pushed the same way. Some need immediate suit. Some need more investigation first. Some need policy analysis before anyone makes another statement. Some require medical development before value can be pressed. Strategy is not just aggression. Strategy is sequencing.

If you are weighing representation, this guide on how to choose a personal injury lawyer is a practical place to start.

One option for Pennsylvania injury cases is Mattiacci Law, a Philadelphia-based personal injury firm that handles serious claims on a contingency basis and prepares cases for trial. Whatever firm you choose, ask direct questions about trial experience, who will handle the case, and how the firm deals with denied claims and coverage disputes.

The right lawyer does not just ask the insurer to be fair. The right lawyer builds a case that makes unfairness expensive.

If the at-fault driver’s insurance company will not pay, do not assume your case is over. A denial can often be challenged with stronger evidence, better use of your own coverage, or litigation that completely changes the dynamic. Mattiacci Law represents injured people in Pennsylvania in serious accident and insurance dispute cases, and the firm offers free consultations and contingency-fee representation for qualifying matters.